For years, Michael Saylor's message never changed: buy Bitcoin, and don't sell. So when Strategy announced the sale of 3,588 BTC, a lot of people took it personally. "The promise has been broken", "the biggest bull has blinked"... some even called it the top.

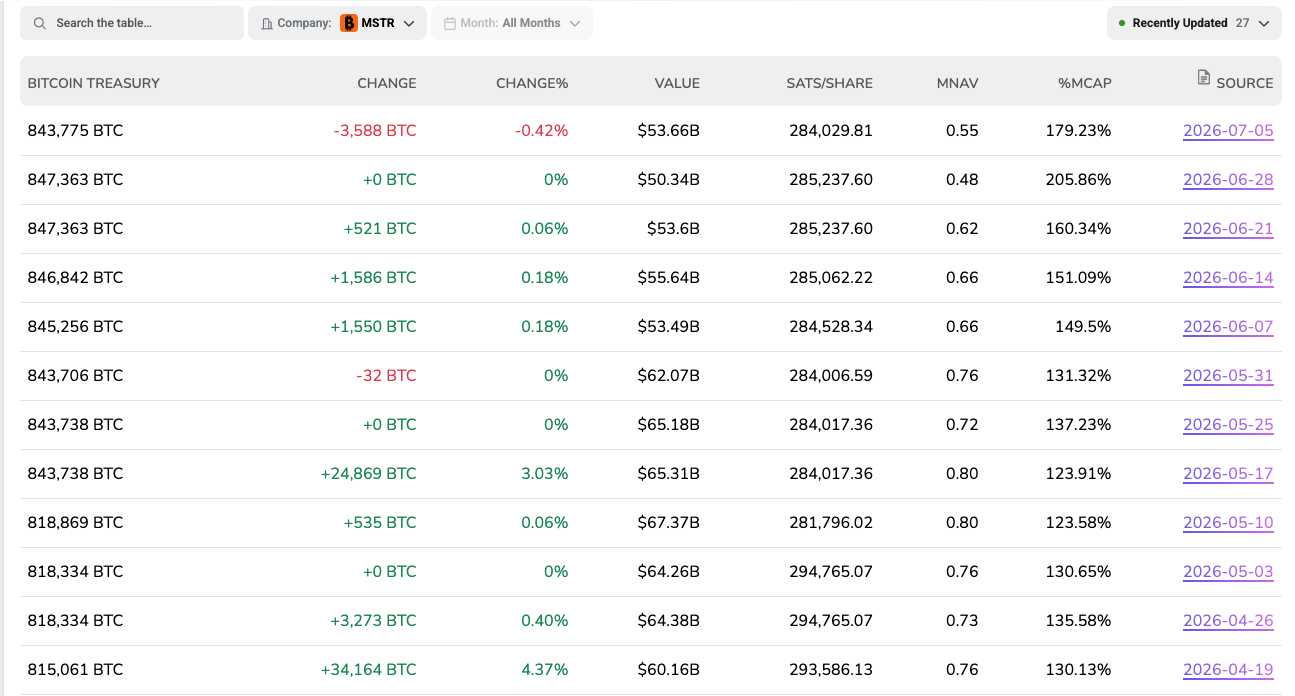

Strategy has sold 3,588 $BTC for $216 million to fund dividends on our Digital Credit securities. As of 7/5/2026, we hodl ₿843,775 in our BTC Reserves and $2.55 billion in our USD Reserves. https://t.co/Cssgz29Psj

— Michael Saylor (@saylor) July 6, 2026

I read it the other way. And once I dug into why the sale happened, it actually made me more comfortable with Strategy.

First, what actually happened

Between June 29 and July 5, Strategy sold 3,588 BTC for about $216 million. It did so in two pieces, and it used the cash for something very specific: paying the dividends on its preferred stock (STRF, STRE, STRK, STRD, and the June payment on STRC) and refilling a cash reserve that now sits at around $2.55 billion.

Yes, it's the largest Bitcoin sale in the company's history. But that's mostly because Strategy has barely sold before and thus any sale would set a record. The size is what matters, so let's look at the size.

0.42% is not a goodbye

Here's the number that should cool the panic down. According to our treasury tracker, Strategy held 847,363 BTC before this sale. So 3,588 coins is 0.42% of their stack. After selling, the company still holds about 843,775 BTC worth roughly $52.9 billion.

If you stop focusing on this week and look at the year as a whole, the story flips completely. Strategy's holdings are up around 41.25% over the past twelve months, and up 25.22% in the last six. This company has been buying, relentlessly, the entire time. So a 0.42% selloff against everything it bought, is not a bull turning bearish.

One more number, because it's the one I keep coming back to: the remaining Bitcoin is worth about 179% of Strategy's entire market cap. The market is currently valuing the whole company at less than the Bitcoin sitting on its balance sheet. Nobody in that position is desperate to sell coins. So the real question isn't "is Strategy dumping?" It clearly isn't. The question is why sell any at all.

The mechanics behind the sale

For quite some time, Strategy's whole machine was built to run one way: when the stock trades at a premium to its Bitcoin, the company issues shares, buys BTC with the cash, and everyone's Bitcoin-per-share goes up. That only works while the premium is there.

Right now the premium is gone and Strategy trades below the value of its Bitcoin. Flip that switch and the logic inverts: issuing new shares to raise cash now dilutes Bitcoin-per-share for the people who already own the stock. The tool that used to reward shareholders starts costing them.

So when a bill comes due, the real question is which funding option does the least damage. Below NAV, selling a small amount of Bitcoin does less damage than printing cheap stock. That's the point Josh Mandell made:

"When the usual approach to funding dividends is just selling more shares of common stock, opting to sell a small amount of Bitcoin instead essentially behaves like a buyback of the common."

Strategy's president, Phong Le, framed the same move as the company "evolving from one-way capital issuance to active capital management."

I'd take the company's phrasing with a grain of salt, management has every incentive to make a forced-looking sale sound like a masterstroke. But the math underneath is real, and it lines up with something I've argued before. I've been skeptical of the pure "hold only" treasury model: a Bitcoin treasury should be "the cherry on top of a well-run business, not the other way round." A treasury that can only ever buy is fragile the second the premium disappears. So a company choosing to trim a sliver of Bitcoin over dumping discounted stock isn't what worries me here, it's the first real test of whether these companies can actually manage a balance sheet, and this time the answer was yes.

The part I'm less sure about: STRC

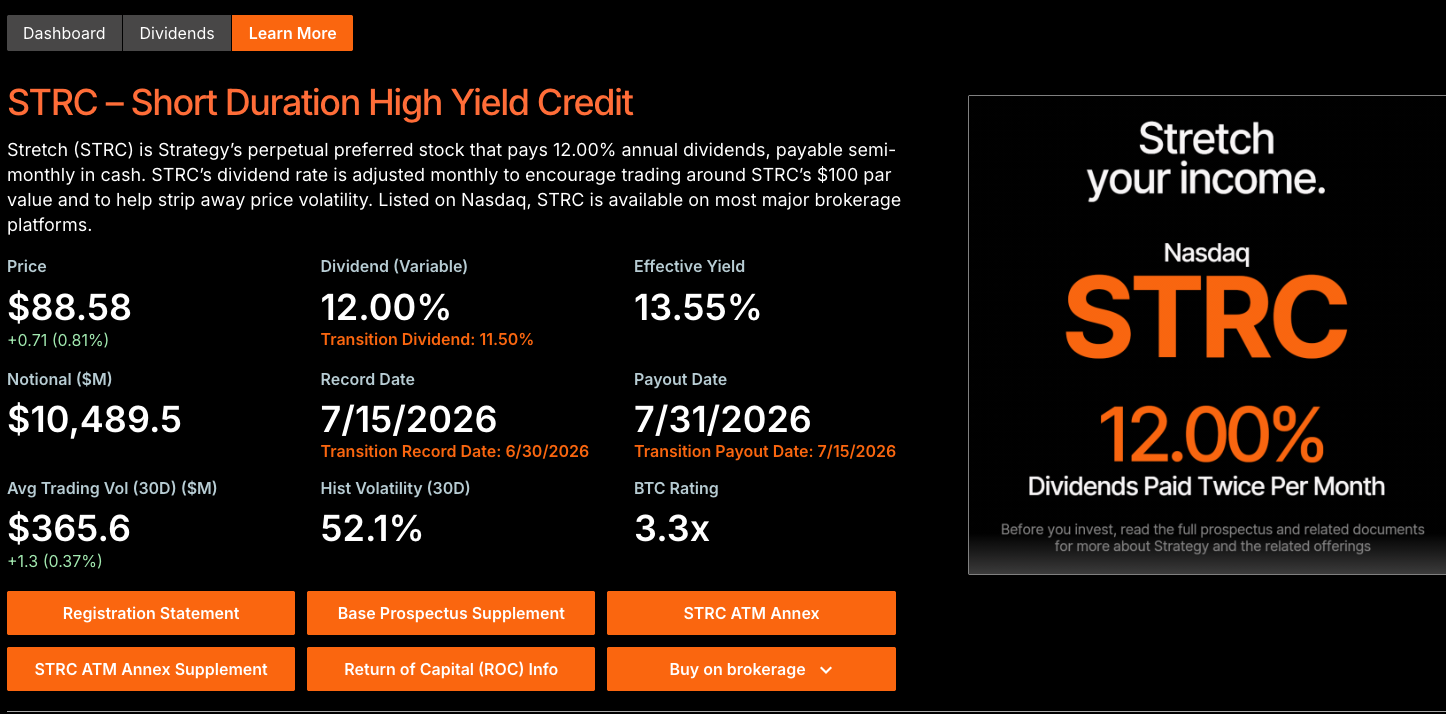

All of this traces back to one thing, the dividends Strategy now has to pay, and the loudest piece of that is STRC.

STRC in plain terms: it is a perpetual preferred share priced around $100, and it now pays a 12% annual dividend, in cash, twice a month. Strategy nudges the rate a little each month to keep the price pinned near $100, so buyers can treat it almost like a high-yield savings account. A nice deal if you're the one holding it.

From Strategy's viewpoint, STRC is a large cash bill that never stops arriving. Here's the catch: the software business underneath doesn't generate enough cash to cover it. So the dividend has to be paid from somewhere else, either by issuing more securities or by selling Bitcoin. That's the entire reason last week's sale happened. The preferred dividends came due, and Bitcoin was the cleanest way to pay them.

I won't pretend to have a strong opinion on whether that 12% is sustainable long-term. STRC is a complicated instrument and I'd rather be honest than hand-wavy. But I know which number to watch: not this quarter's 0.42%, but whether the cash cost of the preferred stack starts growing faster than Strategy can comfortably carry. Paying the dividend on time today is fine. Having to sell steadily bigger chunks of Bitcoin to keep paying it would not be.

Final thoughts

Putting it all together, it is difficult to reach a bearish conclusion. Strategy sold just 0.42% of its total Bitcoin holdings, which are still up 42% compared to the previous year. Its Bitcoin stack is currently worth 179% of the company’s market cap, and the proceeds are being deployed in a way that actually protects shareholders from dilution. Seeing the market’s largest Bitcoin holder show that it can actively manage capital instead of simply hoarding it makes the position more compelling.

As an individual investor, my takeaway is straightforward. This headline by itself is not a sell signal. What matters more is the broader trend. I will continue monitoring the net-flow data on our treasuries dashboard over the coming weeks. If this sale remains an isolated move while other companies keep accumulating, the headline will likely prove to be little more than noise. However, if net flows across corporate treasuries start turning consistently negative, that would be the signal worth paying attention to.

Buy-and-hold made a great story. But knowing when to manage the balance sheet makes a better business.

Disclaimer: The views expressed in this article are my own and are based on publicly available information. This content is intended for informational purposes only and should not be construed as investment advice. Readers are encouraged to conduct their own research before making any investment decisions. Past performance is not indicative of future results.